Let’s talk about what the Breadfast deal reveals about what is broken, not what is working.

Eight years. Nearly $100 million in publicly disclosed capital. 120 million people in the market. And we produced one company at this level.

That is not a success story. That is a proof of concept wrapped in a systemic failure. Let me be specific about the failures.

The Valley of Death is real and it is getting wider

Egypt’s early-stage ecosystem is functional. Accelerators, angel networks, pre-seed capital, there is genuine activity at the $100K–$2M range. The problem begins at $2M–$15M. This is the growth-stage funding gap; the range where a startup needs to hire aggressively, build technology infrastructure, and expand beyond its initial market before it has the metrics to attract institutional growth investors.

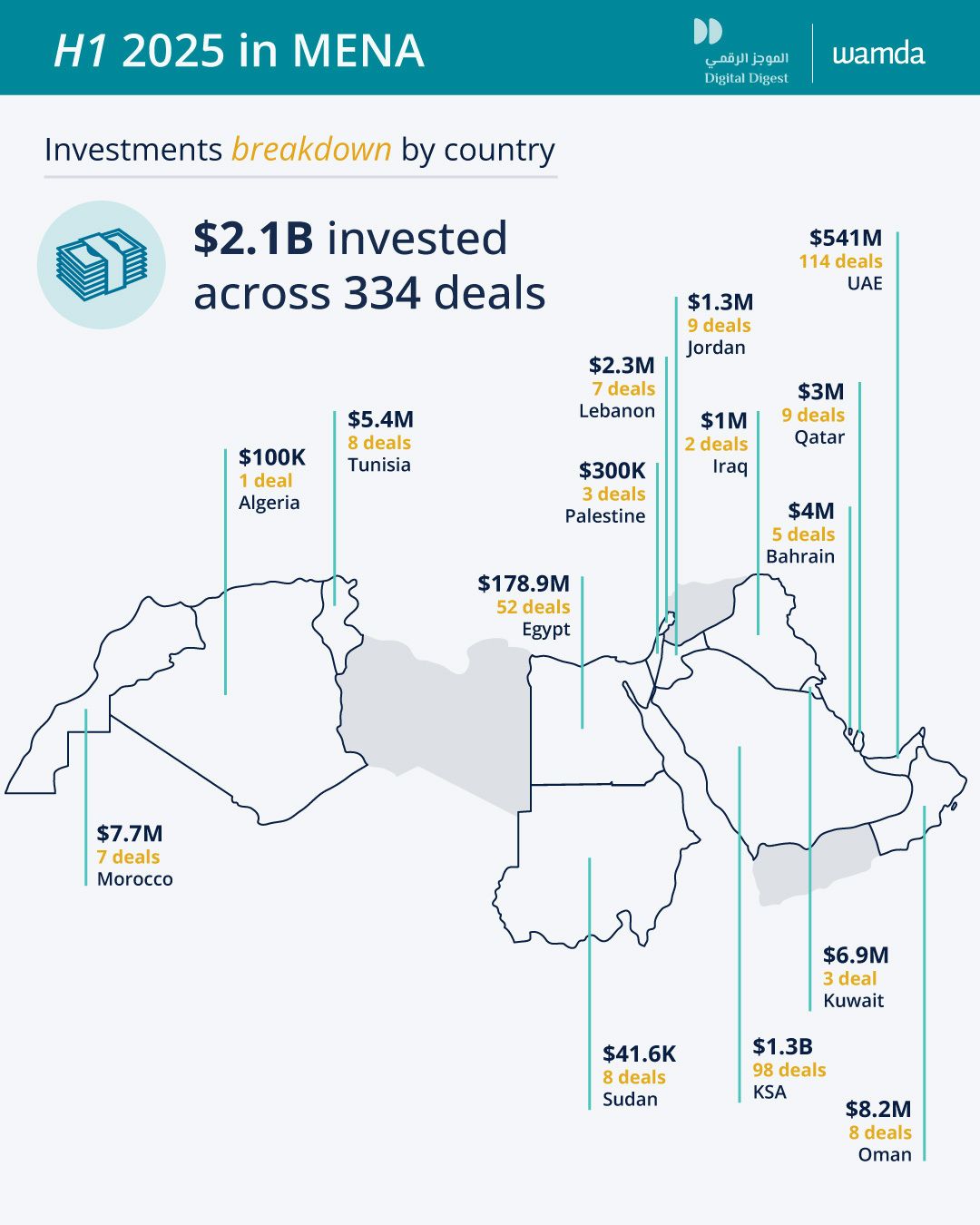

H1 2024 saw Egypt record $86M in total funding across 33 deals; a 75% year-on-year collapse. The average deal size was $2.6M. At that check size, you cannot fund the infrastructure build-out that Breadfast required. The growth-stage capital was simply not present in the Egyptian market in sufficient quantity, at sufficient speed, to support multiple Breadfasts simultaneously.

The exit problem is existential

Venture capital is a recycling machine. Capital flows in, companies grow, exits happen, returns go back to investors, investors reinvest. When the exit market is thin, the machine stops. Egypt has produced two unicorns in its history: Fawry and MNT-Halan. The InfiniLink acquisition by GlobalFoundries in late 2025 was celebrated as a landmark exit. It was. It was also one of the only significant startup exits in recent memory.

Without exits, there are no realized returns. Without realized returns, LPs do not re-up. Without re-ups, funds do not close Fund II. Without Fund II, the capital available for the next Breadfast does not exist. Breadfast’s $50M raise did not happen because the Egyptian ecosystem produced it. It happened despite the ecosystem’s structural limitations, funded largely by foreign capital that came in because the company’s metrics justified it, not because the infrastructure around it was functional.

The currency risk is a structural veto

Every international investor who looked at an Egyptian startup between 2022 and 2024 asked the same question: what happens to my dollar return when the pound devalues? The answer, for most Egyptian startups with EGP-denominated revenue and USD-denominated capital, was devastating. The 70% pound devaluation in 2022–2024 did not just hurt consumer purchasing power. It destroyed the dollar-equivalent value of every EGP revenue line in every Egyptian startup’s financial model.

Breadfast survived this because its GMV retention was so strong that the customer base actually expanded in real terms even as the currency collapsed. Most Egyptian startups at growth stage do not have this characteristic. The currency risk is not a temporary problem. It is a structural feature of building in Egypt that requires either dollar-denominated revenue, hedging strategies, or a much longer investment horizon than most VC models support.

The ecosystem celebrating survival rather than scale

Perhaps the most corrosive pattern in Egypt’s startup ecosystem is the tendency to celebrate survival milestones as if they were growth milestones. A startup that raised a round during the 2022–2024 funding freeze is celebrated. A startup that kept its team through inflation that peaked at 38% in September 2023 is celebrated. A startup that maintained unit economics through a 70% currency devaluation is celebrated.

These are genuinely difficult things to do. But celebrating them as exceptional obscures the fact that they are the minimum requirement for a functional startup ecosystem. In the US, or Singapore, these would not be news. They would be the baseline expectation.

Breadfast’s $50M is a mirror held up to the ecosystem. What it reflects is not just the company’s excellence. It reflects 8 years of underfunding, structural dysfunction, and systemic talent and capital constraints that required an extraordinary team to overcome. The celebration is warranted. The systemic change it demands is more urgent than the celebration suggests.

Breadfast’s $50M is worth celebrating. It is also worth being honest about: one extraordinary company does not fix a broken ecosystem.

The structural problems described in this post; the Valley of Death, the funding cliff at growth stage, the currency risk veto on international capital, will still be there the day after the celebration ends.

My challenge to every fund manager, accelerator, government official, and institutional investor operating in the Egyptian ecosystem: what is the one structural change; regulatory, financial, or behavioral, that you believe would do the most to prevent the next Breadfast from being the only Breadfast? Tell me in the comments. I’ll compile the most substantive answers into a follow-up post.

Missed the first 4 articles? Read them here:

- The Deal: What Breadfast’s $50M Round Actually Signals

- Mostafa Amin Failed 4 Times Before Breadfast. That’s Not a Backstory. That’s the Point.

- 40% of Breadfast’s Sales Are Private Label. Nobody Is Talking About What That Actually Means.

- Breadfast Started With Bread. It’s Building Toward Money. We’ve Seen This Movie Before.

References

1) Breadfast. “Breadfast raises $50 million pre-Series C round backed by international institutional investors to scale consumer supply-chain infrastructure.” https://www.breadfast.com/blog/breadfast-raises-50-million-pre-series-c-round-backed-by-international-institutional-investors-to-scale-consumer-supply-chain-infrastructure-breadfast-raises-50-million-pre-series-c-round-backed-by-international-in/?srsltid=AfmBOorgxxaQrJ46WzFWAxlH6nolvHMua_pMtCbXzr1-u5FPkD08Qjff

2) European Bank for Reconstruction and Development (EBRD). “EBRD backs Egyptian e-grocer Breadfast.” https://www.ebrd.com/home/news-and-events/news/2026/us–10-million-to-breadfast-egypt.html

3) International Finance Corporation (IFC). “Breadfast Equity” project disclosure / proposed investment materials. https://disclosures.ifc.org/project-detail/ESRS/52184/breadfast-equity

4) MAGNiTT. “H1 2024 Egypt Country Insights Report.” https://magnitt.com/research/h1-2024-egypt-country-insights-report-50950

5) Forbes Middle East. “Egypt’s VC Market Sees 75% Drop In H1 Funding: Report.” https://www.forbesmiddleeast.com/innovation/startups/egypts-venture-capital-markets-total-funding-in-h1-2024-dips-75-to-%2486m-says-report

6) MAGNiTT. “FY2024 Egypt Venture Investment Country Insights.” https://magnitt.com/research/fy2024-egypt-venture-investment-premium-report-50981

7) MAGNiTT. “The Problem of Exits in MENA.” https://magnitt.com/research/The-Problem-of-Exits-in-MENA-51009

8) Egypt Ventures. “Egypt Ventures Announces Successful Exit from InfiniLink to GlobalFoundries, Underscoring Egypt’s Growing Deep-Tech Innovation.” https://egyptventures.com/egypt-ventures-announces-successful-exit-from-infinilink-to-globalfoundries-underscoring-egypts-growing-deep-tech-innovation/