من ضغوط الاقتصاد إلى مرحلة “إعادة بناء” حقيقية

على الرغم من استمرار الضغوط الاقتصادية، فإن ما يحدث في مصر اليوم أقرب إلى إعادة بناء المنظومة من جديد، لا مجرد تعافٍ مؤقت. وبرأيي، قد تكون 2026 عامًا مفصليًا: من يبني الآن على أسس صحيحة، سيحصد أفضلية واضحة مع موجة النمو المقبلة.

أين تقف مصر اليوم إقليميًا وعالميًا؟

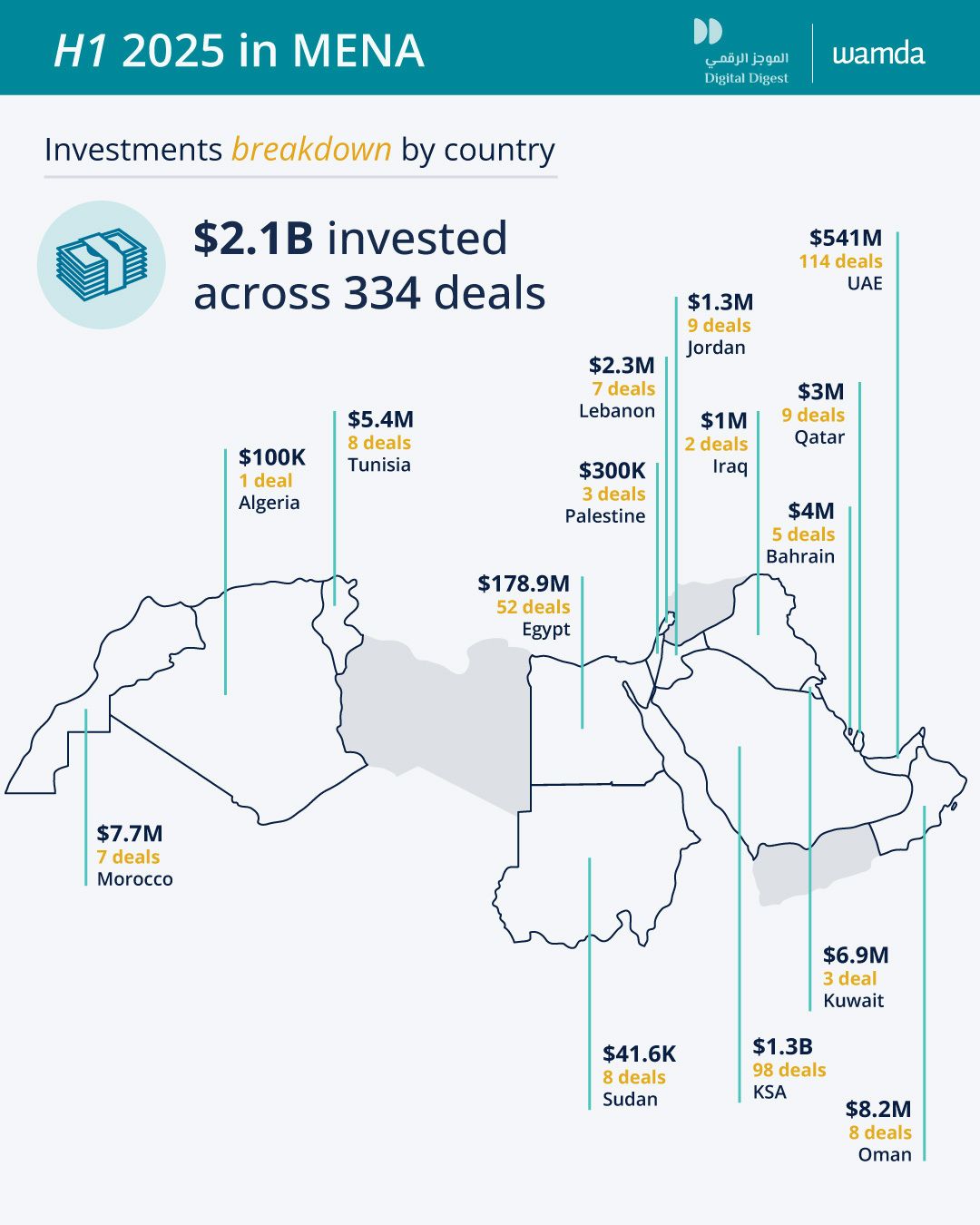

أصبحت مصر ضمن أكبر ثلاث منظومات تمويل للشركات الناشئة في منطقة الشرق الأوسط وشمال أفريقيا، وتقدمت إلى المركز 65 عالميًا في مؤشر منظومات الشركات الناشئة بعد أن كانت في المركز 81 عام 2020.

كما يتسم المشهد بتمركز شديد في العاصمة:

- القاهرة تضم نحو 90% من الشركات الناشئة النشطة

- أكثر من 600 شركة ناشئة (نشطة وقيد التشغيل)

- ويُقدَّر حجم “الاقتصاد الريادي” بحوالي 8.3 مليارات دولار

هذا التركّز يحمل ميزة واضحة في تجميع رأس المال والمواهب والشبكات في نقطة واحدة، لكنه في الوقت نفسه يكشف فرصة كبيرة لمحافظات أخرى إذا توفرت لها مقومات التمكين.

القطاعات الأكثر تأثيرًا في مصر حاليًا

يمكن تلخيص المشهد في ستة قطاعات تحمل الثقل الأكبر:

- التقنية المالية FinTech

لأنها تعالج تحديات الدفع والائتمان والشمول المالي في سوق ضخم واحتياجه واضح. - التجارة الإلكترونية E-commerce

ليس كمتاجر رقمية فقط، بل كبنية تشغيل: سلاسل إمداد، تشغيل، مدفوعات، وتجربة عميل. - اللوجستيات والتنقل Logistics & Mobility

الفرصة هنا لمن يحوّل الفوضى إلى نظام: كفاءة، تتبع، جدولة، وخفض تكلفة. - التقنية الصحية HealthTech

الطلب كبير، والفرص في الخدمات القابلة للتوسع: تشخيص مبكر، متابعة، ورعاية رقمية. - التقنية التعليمية EdTech

سوق واسع، والتحدي الحقيقي هو نموذج ربحي مستدام بعيدًا عن “التمويل المؤقت”. - البرمجيات والذكاء الاصطناعي Software & AI

قد تكون الموجة الأقوى، لكن النجاح ليس في “الذكاء الاصطناعي” كعنوان، بل في منتج يحل مشكلة تشغيلية واضحة ويدخل ميزانيات حقيقية.

التمويل: قفزة كبيرة، ثم تصحيح، ثم عودة تدريجية للتوازن

إذا نظرنا إلى التمويل في صورة كلية:

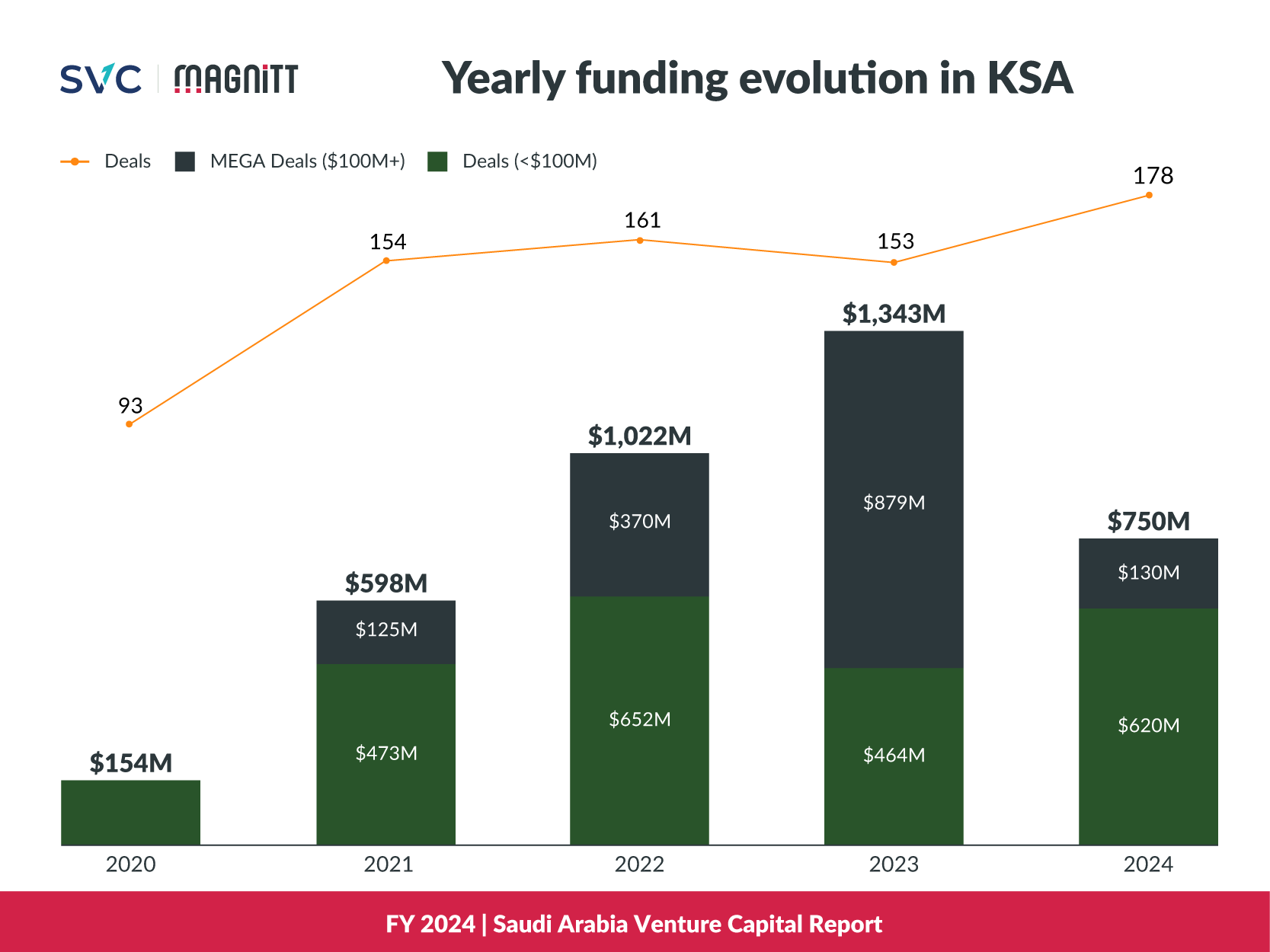

- من 2015 إلى 2019: نحو 314 مليون دولار

- من 2020 حتى اليوم: نحو 2.2 مليار دولار

أي أن حجم التمويل تضاعف بأكثر من 7 مرات خلال خمس سنوات.

لكن الأهم هو شكل الدورة التمويلية نفسها:

- 2021 و2022 شهدا طفرة واضحة

- 2023 و2024 شهدا “تصحيحًا” خصوصًا في الجولات الصغيرة والمتوسطة

- 2024 كان عامًا انتقاليًا: نحو 300 مليون دولار في 78 صفقة

ثم بدأت مؤشرات التحسن في 2025 بشكل أوضح:

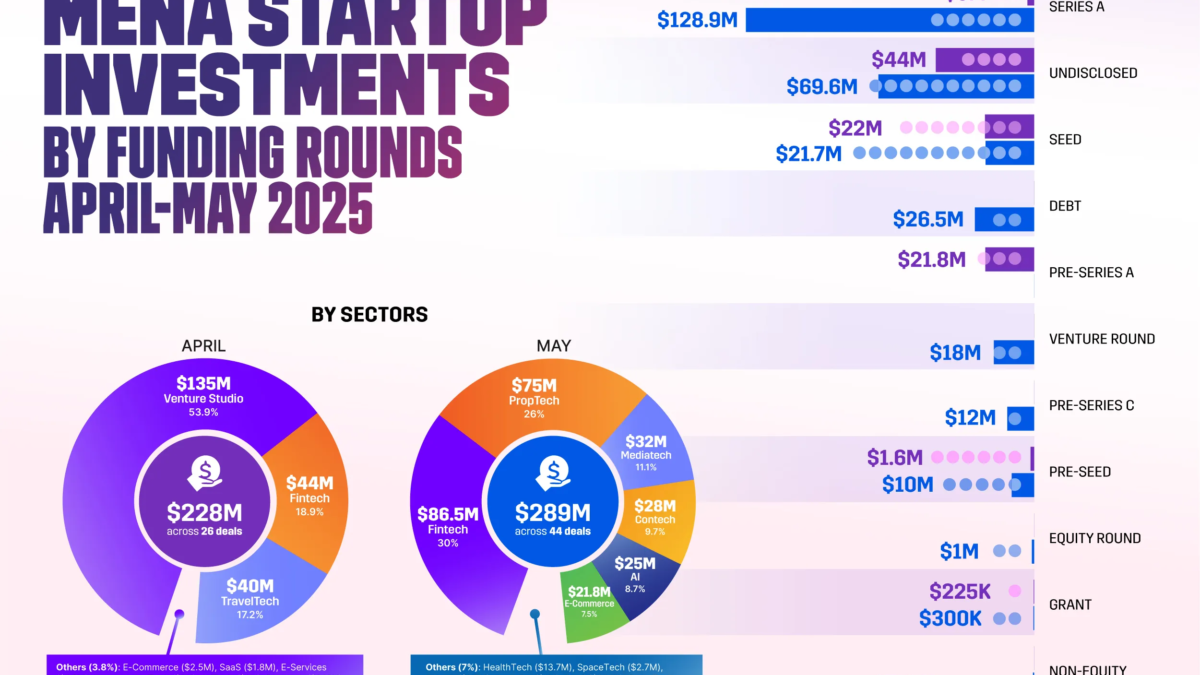

في أول خمسة أشهر فقط، جمعت الشركات الناشئة المصرية نحو 228 مليون دولار في 16 صفقة، بزيادة تقارب 130% مقارنة بالفترة نفسها من 2024، مع صفقات كبيرة مثل:

- Nawy في قطاع PropTech بنحو 75 مليون دولار

- وتمويل ديون جديد لـMNT-Halan التي تُعد أول شركة مصرية “يونيكورن”

النمو عاد، لكن بمعايير أكثر صرامة. السوق لم يعد يكافئ “النمو بأي ثمن”.

دعم حكومي: تغييرات تنظيمية قد تعيد رسم قواعد اللعبة

هناك حراك حكومي ملحوظ لدعم الشركات الناشئة، من أبرز ملامحه:

- تقليل مدة تأسيس الشركة من أكثر من 40 يومًا إلى نحو 11 يومًا

- إعفاءات ضريبية للشركات التي تقل مبيعاتها عن 20 مليون جنيه

- إعداد “ميثاق الشركات الناشئة” Startup Charter لتبسيط التعامل مع الجهات الحكومية

- وفي 2025، تخصيص منطقة حرة تكنولوجية جديدة بمساحة تقارب 9000 متر لدعم شركات الذكاء الاصطناعي والتقنية المالية والبرمجيات

هل هذا كافٍ؟ ليس بعد.

لكن استمرار التنفيذ في هذا الاتجاه يقلل الاحتكاك التشغيلي ويرفع قابلية النمو.

لماذا تبدو 2026 “مختلفة” فعلًا؟

لأنها تبدو سنة فرز حقيقي.

النجاح لن يكون لمن “يجمع جولة تمويل” فقط، بل لمن يستطيع أن:

- يبني منتجًا يُباع ويستمر

- يضبط اقتصاديات الوحدة مبكرًا

- يضع مسار توسع إقليمي واضح

- يبني حوكمة وامتثالًا من البداية

- يصنع ميزة تنافسية يصعب نسخها

وبالنسبة للمستثمرين، فالتقييمات أصبحت أكثر واقعية، والسوق بدأ يكافئ الجودة والصلابة التشغيلية بدل الضجيج.

مصر كبوابة للمنطقة: فرصة كبيرة لكنها ليست تلقائية

إذا استمر مسار الإصلاح، ومع استمرار نمو التمويل بالوتيرة الحالية، يمكن لمصر أن تظل:

- بوابة رئيسية لمنطقة الشرق الأوسط وشمال أفريقيا

- سوقًا ضخمًا للاختبار والتحقق من المنتج

- مصدرًا مهمًا للمواهب التقنية

ومع الوقت قد نشهد “يونيكورن” جديدة في قطاعات مثل: PropTech، والتجارة بين الشركات B2B، والتقنية المالية.

السؤال الحقيقي

المشهد يُعاد بناؤه… والفرصة واضحة.

من سيستغل هذه اللحظة لبناء شركات تستطيع أن تنمو وتربح فعليًا على مستوى الإقليم؟

المراجع:

[1] WTO (World Trade Organization) – Egypt | ICT Services Export Promotion (PDF).https://www.wto.org/english/tratop_e/ts4d_e/case_studies_e/egypt.pdf

[2] StartupBlink – Egypt Startup Ecosystem (Rankings, Startups, Insights).https://www.startupblink.com/startup-ecosystem/egypt

[3] StartupBlink – Cairo Startup Ecosystem (Rankings, Startups, Insights).https://www.startupblink.com/startup-ecosystem/cairo-eg

[4] EnterpriseAM – Egypt leads startup activity in Africa in 2024 (Jan 12, 2025).https://enterpriseam.com/egypt/2025/01/12/egypt-leads-startup-activity-in-africa-in-2024/

[5] Ministry of Planning, Economic Development and International Cooperation (Egypt) – Egyptian Startups Attract $228M (Jan–May 2025) (Jun 1, 2025).https://www.mped.gov.eg/singlenews?id=6324&lang=en

[6] Wamda – Nawy secures $75 million in equity, debt to fuel MENA expansion (May 12, 2025).https://www.wamda.com/2025/05/nawy-secures-75-million-equity-debt-fuel-mena-expansion

[7] Reuters – Egypt’s MNT-Halan says Turkish acquisition… (Jul 31, 2024). [8] The Egyptian Entrepreneurship Sector Diagnostics Report 2023 By Entlaq Holding